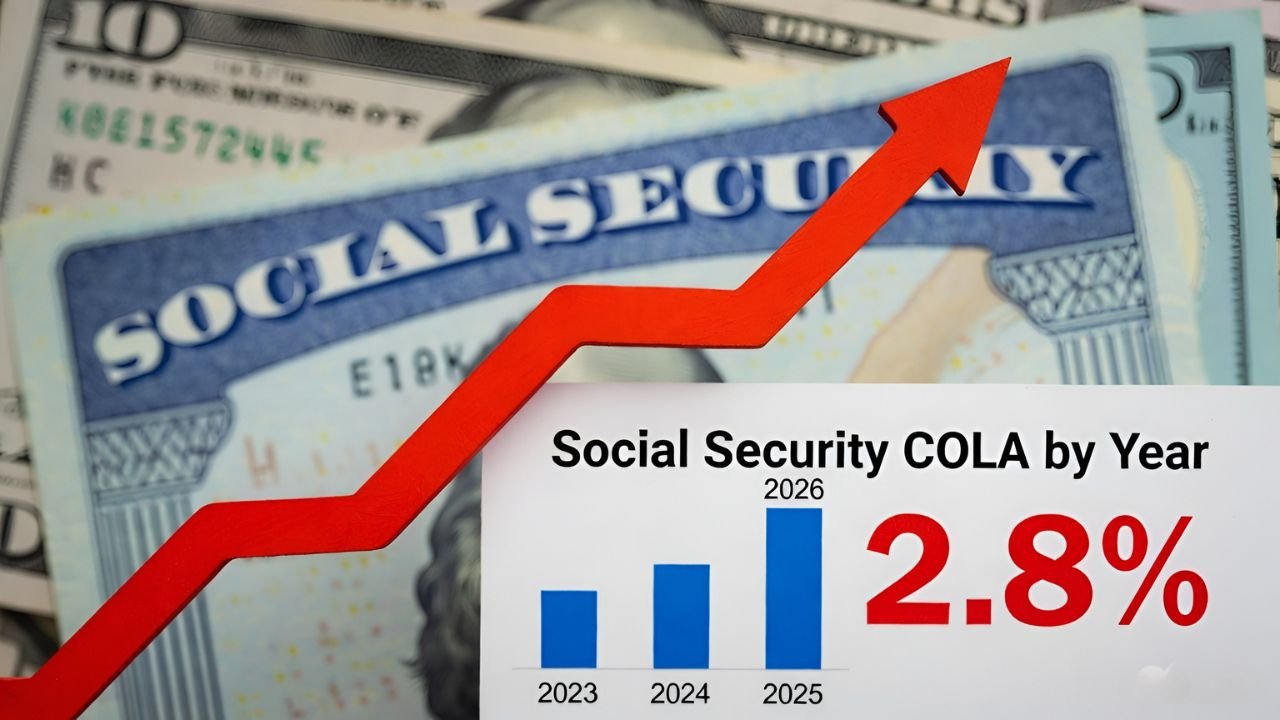

The cost-of-living adjustment (COLA) in social security 2026 is likely to be the greatest increase in social security in recent years. It is projected to be between 2.7% and 2.8 percent which is a little higher than the 2.5 percent growth in 2025. This news appears to be a blessing at the beginning because of millions of retired Americans who depend on Social Security as a major source of their monthly wages. As an illustration, an average person may have an earning of 1700 dollars monthly, and a 2.8 per cent growth will result in an extra 48 to 50 dollars. Earners with an average monthly income of approximately 2,008 are likely to experience a net growth of approximately 54 to 56.

The question is though, will this rise be in a position to match the rising inflation?

Medicare Premiums: This is where the bulk of the increase will be spent

It is estimated that Medicare Part B premiums will grow by about 11.5 percent in 2026 and the monthly premiums will rise to about 206. This will take up much of the increase in the COLA since this premium will be deducted directly out of Social Security payments. It will be estimated that up to 40 percent of the COLA increment will be expended just on higher Medicare premiums.

This implies that in case an individual is given a raise of 54, he/she might only be left with just 32-33. As a result of this, this historic touted increase might be restricted to paperwork.

Inflation and Rising Costs of Living

The COLAs are computed using Consumer Price Index (CPI-W) which is used to evaluate the cost of urban workers and clerical employees. Nevertheless, this index is not supposed to be a full picture of the real costs of seniors as many experts think. Basic needs are largely increased in cost, particularly healthcare, medication, rent, electricity, water, and food.

Although there are recent announcements of large COLA growth, as 5.9% in 2022 and 8.7% in 2023, many retirees did not feel that their purchasing power improved substantially. The cause is obvious: the costs are increasing at a higher rate than the revenues.

[also_read id=”2437″]

A “Double Whammy” Situation

On the one hand, economists refer to it as a two-punch blow, that is, limited COLA adjustments and, on the other, the skyrocketing costs. This scenario puts mental and financial strain on the retirees. This is compounded even to those who do not have extra savings or a pension.

Moreover, the full retirement age of individuals born in 1959 will go up to 66 years and 10 months. It is also likely that the taxable wage limit and early retirement earnings limit will be changed which would further raise the overall financial burden.

Possible Solutions for Low-Income Individuals

There are some proposals in the policy arena which may alleviate the burden of low-income benefit recipients. These involve greater subsidies on premiums and Part B and Part D of Medicare, limits out-of-pocket expenditure and simplification of low-income subsidy programmes. When these measures are put in place properly the real worth of COLAs might be passed through to beneficiaries in a better way.

[also_read id=”2472″]

What’s the Way Forward?

Financial analysts suggest that seniors should re-analyze their budgets, think about other sources of income, and, hopefully, postpone their Social Security benefits to get higher monthly checks. This financial strain can also be countered in a way with proper planning and information.

Finally, the COLA raise in 2026 will definitely be welcome, yet it is also true that this relief will likely be very short-lived in the context of increasing healthcare expenses and inflation. Receiving a rise is not the only problem that retirees have to face, but to be able to preserve their purchasing power.